Hey there,

Today I want to talk about financing. It’s the part of the storage business that most operators underestimate until it bites them. I’ve seen great assets in bad capital structures lose everything. I’ve also seen average assets in smart capital structures generate wealth through two recessions, a pandemic, and the fastest rate cycle in 40 years. Today’s newsletter is all about how to structure your financing so the market’s problems become your opportunities - and not the other way around.

Understanding Leverage in Self-Storage

Leverage is the most powerful tool in real estate finance. It amplifies returns when markets are favorable and amplifies risk when they’re not. The question is never whether to use it — it’s how much, at what terms, and with how much cushion built into your structure.

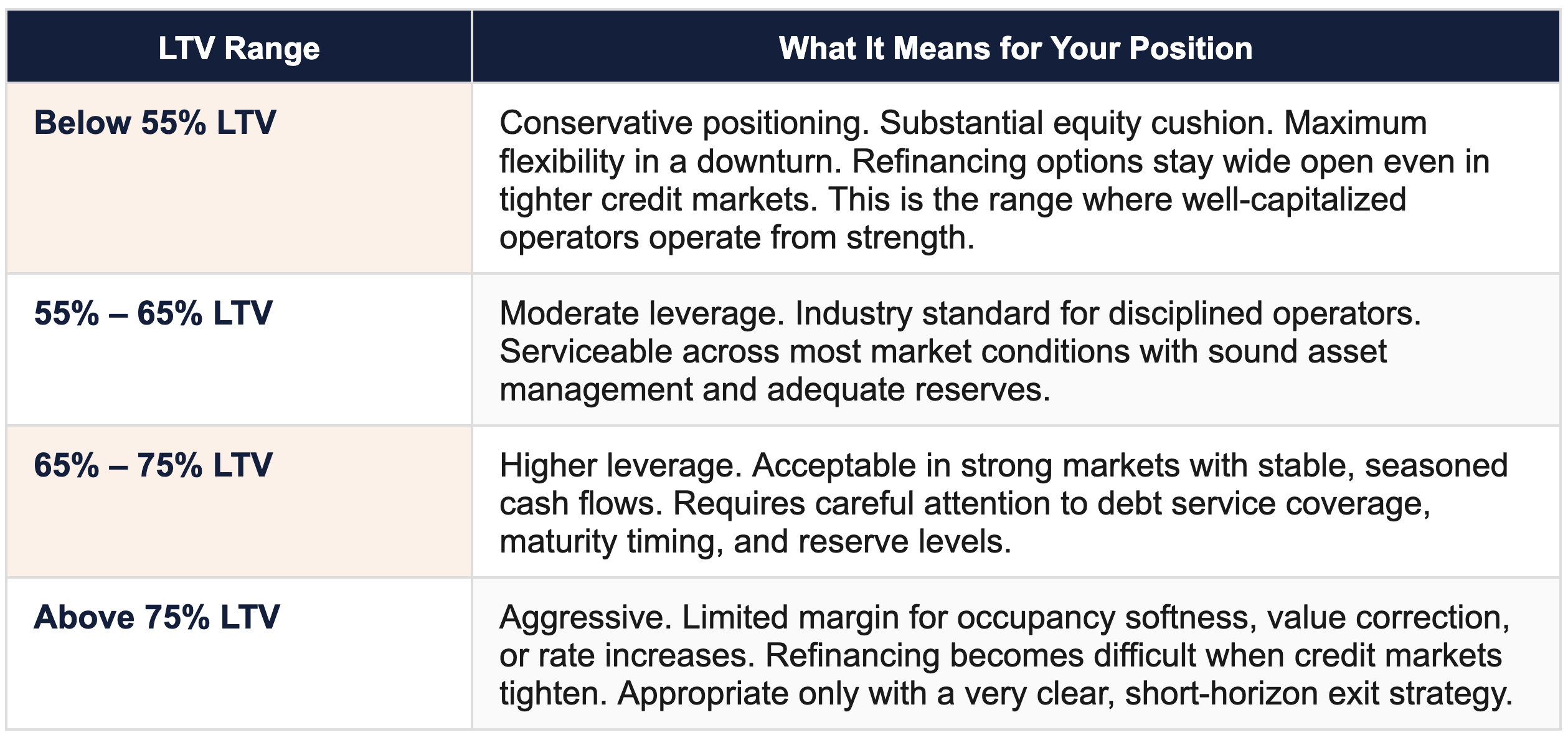

Loan-to-Value: Where Every Conversation Starts

Loan-to-value (LTV) is the ratio of your debt to your asset’s estimated value. It tells you two things at once: how much equity cushion you’re sitting on, and how much room the market has to move before your capital structure becomes a problem.

Here’s a practical framework for how to think about LTV ranges in self-storage:

*An important exception to point out here is SBA loans. SBA loans are generally higher leverage at 85-90% LTV and can be great opportunities for first time buyers. Having said that, when using higher leverage it's important to have a strong business plan in place so you can execute on a plan that allows you to hit the target DSCR numbers that the bank requires. Generally speaking, SBA loans are more often used when there is a clear value-add opportunity to increase the net operating income through operational improvements, expansion opportunities, etc.

For reference: Cedar Creek Capital’s portfolio weighted average LTV is 56.8% across 21 properties as of January 2026. That number reflects a deliberate operating philosophy: carry enough equity in every asset that a shift in market conditions creates an option to act, not an obligation to react.

The operators who got squeezed in 2022–2024 weren’t necessarily paying too much for assets. Many were in the wrong structure at the wrong leverage level at the wrong time. LTV alone doesn’t tell the whole story - but it’s always where the story starts.

Debt Service Coverage Ratio (DSCR): The Other Number That Matters

DSCR measures how many times your net operating income covers your debt payment. A 1.0x DSCR means your income exactly covers your debt service - no cushion whatsoever. Most lenders require 1.20x to 1.25x at origination.

What lenders require and what you should target are two different numbers. A facility running at 1.15x DSCR has essentially no margin if occupancy softens 5%, expenses spike, or your rate adjusts. Target 1.30x or higher at origination and model your downside before you close.

Stress-Test Before You Sign

Before committing to any loan, run three scenarios: (1) Current market conditions. (2) 10% drop in occupancy. (3) 200 basis point rate increase on any floating exposure. If scenario 3 puts you below 1.10x DSCR, reconsider the structure - not just the deal.

Matching Your Debt to Your Strategy

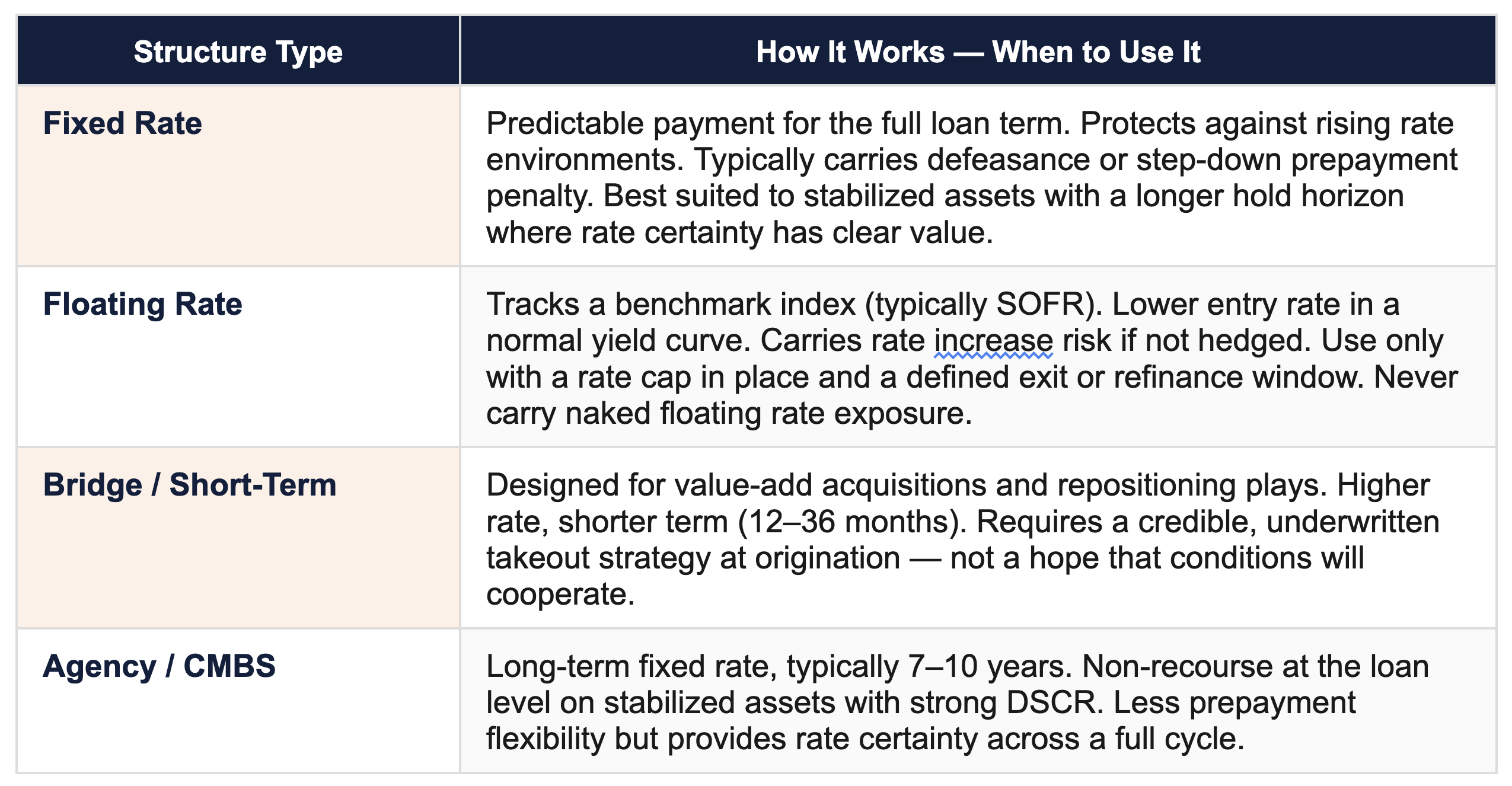

The structure of your loan - its rate type, term, amortization schedule, and prepayment provisions - determines how your financing performs across a full market cycle, not just at the moment of acquisition. Getting the structure right is as important as getting the rate right.

Fixed vs. Floating Rate: The Decision That Shapes Everything

The 2022–2024 period gave every storage operator a live education in rate risk. The Federal Reserve moved from near-zero to over 5% in roughly 18 months - the fastest rate cycle in 40 years. Simultaneously, a wave of new supply hit major markets as projects permitted at the peak delivered. Operators with floating-rate exposure and no hedge found themselves in serious difficulty through no fault of their acquisition thesis.

The lesson is not to avoid floating rate debt. It is to structure it with explicit downside protection, a clear refinance runway, and enough DSCR headroom to absorb movement before you need to act.

A great deal in a bad capital structure is still a bad deal. Structure the debt for the worst plausible scenario and let the upside take care of itself.

Loan Term and Maturity: The Strategy No One Talks About Enough

When your debt comes due matters as much as what rate it carries. A loan maturing at the bottom of a credit cycle forces a refinancing conversation you didn’t choose, in conditions you didn’t underwrite for.

-

Stagger maturities across your portfolio. If all your loans come due in the same 12-month window, you’re fully exposed to whatever that credit environment happens to be. Spread maturities deliberately.

-

Match term to business plan. Value-add acquisitions being repositioned in 24 months should not be in 10-year paper. Core stabilized assets should not be in short-term bridge debt.

-

Understand every extension option in your loan documents. Extension conditions, fees, and rate adjustments need to be understood before you need them - not when you’re 60 days from maturity.

-

Begin refinance conversations 12 to 18 months before maturity. Credit markets can shift faster than loan calendars. Starting early creates options. Starting late removes them.

Working the Rate Environment You Have

Operators cannot control interest rates. What they can control is how much rate risk they carry, how they protect against adverse moves, and — most importantly — how they position themselves to capitalize when the environment shifts.

Rate Caps: Non-Negotiable on Floating Exposure

A rate cap limits how high your rate can go on floating-rate debt. If you carry any floating exposure, a cap is not optional - it is foundational risk management. Three things to get right:

-

Strike rate: set at a level where your DSCR remains serviceable under the cap scenario, not at the most favorable projection.

-

Term: must match your exposure window without gaps. A cap that expires 6 months before your loan matures leaves you exposed precisely when you can least afford it.

-

Cost: rate caps have become meaningfully more expensive as volatility has increased. Model the cap cost into your acquisition underwriting from day one — it is a real cost of capital, not an afterthought.

How Rate Cycles Create Opportunity

Rising rate environments that stress over-leveraged operators create acquisition opportunities for well-capitalized ones. When operators with weak capital structures are forced sellers, well-positioned buyers can acquire assets at prices that compress years of organic value creation into a single transaction.

This dynamic has played out in every cycle since commercial real estate has been an institutional asset class. Cedar Creek Capital has operated through multiple rate cycles since before 2008. Each one produced both stress and opportunity. The operators who captured the opportunity consistently shared one characteristic: their existing capital structure gave them the liquidity, the lender confidence, and the equity to move.

The Position Advantage

A portfolio at 56.8% average LTV, with intact lender relationships and no capital call history, enters a distressed acquisition market from a position of strength. Lenders extend credit to operators they trust. Equity is available. When over-leveraged operators are reacting to conditions, well-structured operators are acting on them. Surviving a cycle is the floor. Thriving through it is what conservative structure makes possible.

Refinancing as Active Capital Management

Refinancing is not just a maturity response - it is a lever for building long-term portfolio value. Consider refinancing proactively when:

-

Rates drop meaningfully below your current loan rate and the prepayment penalty math works in your favor over a reasonable hold horizon.

-

Asset appreciation has created equity you can extract and redeploy into acquisitions, capital improvements, or portfolio rebalancing.

-

Loan terms have become misaligned with your current plan due to market changes, asset performance, or an evolution in your strategy.

-

Improved lender relationships can access better covenants, terms, or structures than what was available at origination.

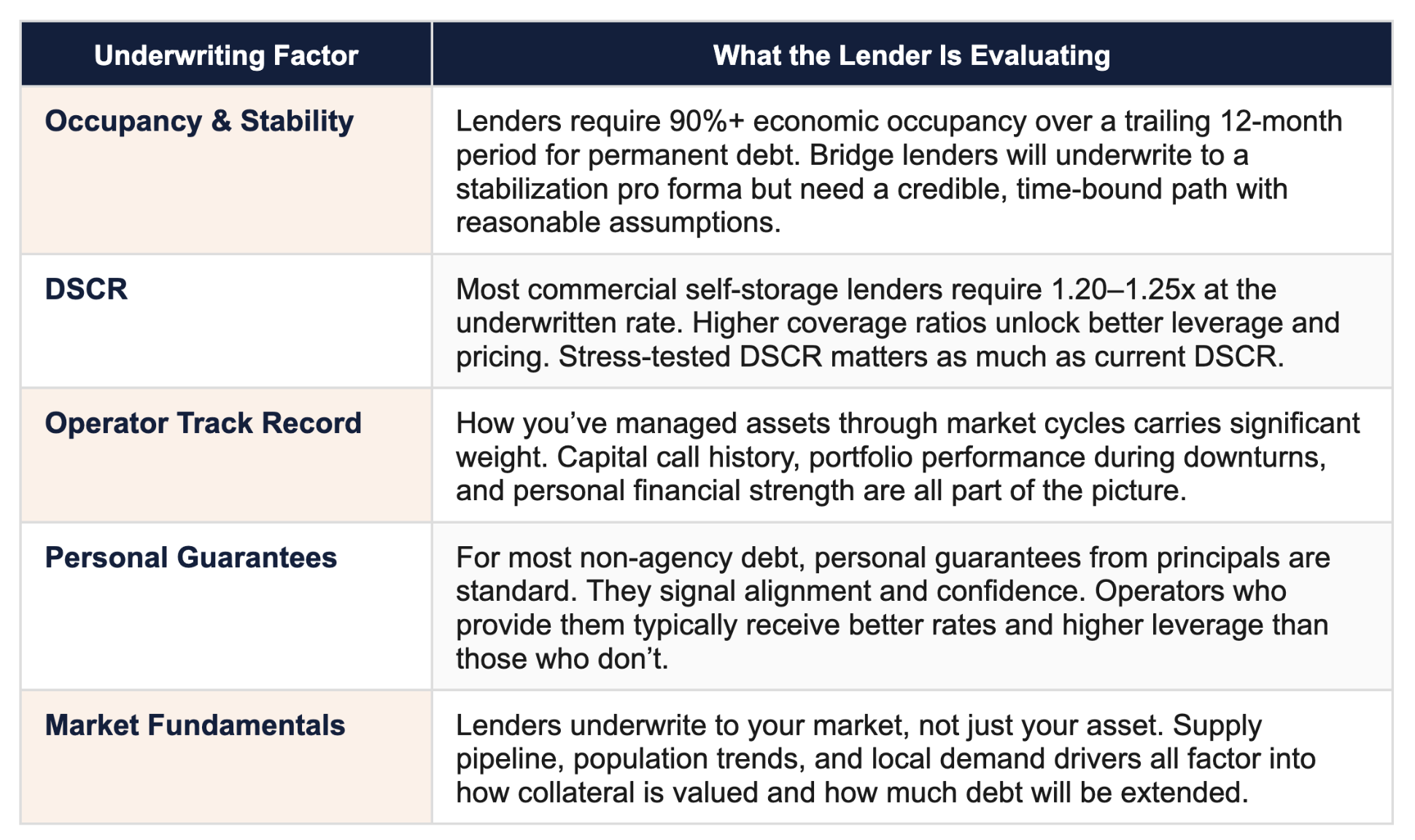

What Lenders Are Actually Evaluating

Understanding how lenders underwrite self-storage loans helps operators structure transactions to succeed at credit approval - and build the kind of lending relationships that provide access to capital across market cycles.

Personal guarantees deserve emphasis. Many operators try to structure around personal liability. The practical outcome is typically worse loan terms, lower leverage availability, and weaker lender relationships - precisely the opposite of what operators trying to protect themselves actually achieve.

The operators with the strongest lender relationships are almost always the ones who provide personal guarantees, maintain conservative leverage, and have a clean history of managing assets without asking their partners - lenders or investors - to absorb their problems.

Your lending relationship is a long-term asset. How you manage your capital structure today determines what your lender will offer you the next time you need them - especially when conditions aren’t perfect.

Surviving Cycles. Thriving Through Them.

The difference between operators who survive market downturns and those who thrive through them is almost never the quality of their assets. It is the flexibility built into their capital structure before conditions changed.

Surviving means you don’t lose assets. Thriving means your structure allows you to acquire when others are selling, refinance when others can’t, and build through a downturn instead of managing through one.

Rule 1: Never Finance to Capacity

The maximum leverage a lender will extend is a ceiling, not a target. Finance to a level that leaves room for the asset’s performance to soften before the capital structure becomes the problem. What looks conservative at origination looks prescient at the bottom of a cycle.

A useful discipline: before closing any loan, ask what happens to this deal if occupancy drops 10% and rates rise 200 basis points simultaneously. If the answer is distress, the structure needs to change.

Rule 2: Build a Structure That Works Across Scenarios

Capital structures that require a specific refinancing window, a specific cap rate environment, or a specific exit timing to function are fragile. Every financing decision should be stress-tested against a range of outcomes, and the structure should remain functional across all of them.

In practice, this shows up in one metric above all others: capital call history. In over 20 years of operating self-storage through multiple market cycles - including 2008, COVID, and the 2022–2024 rate environment - Cedar Creek Capital has never issued a capital call. Every shortfall was covered by the principals personally. That record is not luck. It is the result of conservative leverage decisions made at origination, before market conditions required anything of the capital structure.

Rule 3: Liquidity Is a Competitive Weapon

Available liquidity - cash reserves, unused credit capacity, equity in existing assets - is what separates operators who can move quickly in a distressed market from those who watch from the sideline. Every point of excess leverage carried during good markets reduces the liquidity available to deploy during bad ones.

The operators who look the most aggressive in hindsight - the ones making acquisitions at the bottom, building portfolios during downturns - are almost always the ones who looked the most conservative on the way up.

Leverage without flexibility is the most expensive thing you can own. The goal is a capital structure where market stress creates options for you, not obligations.

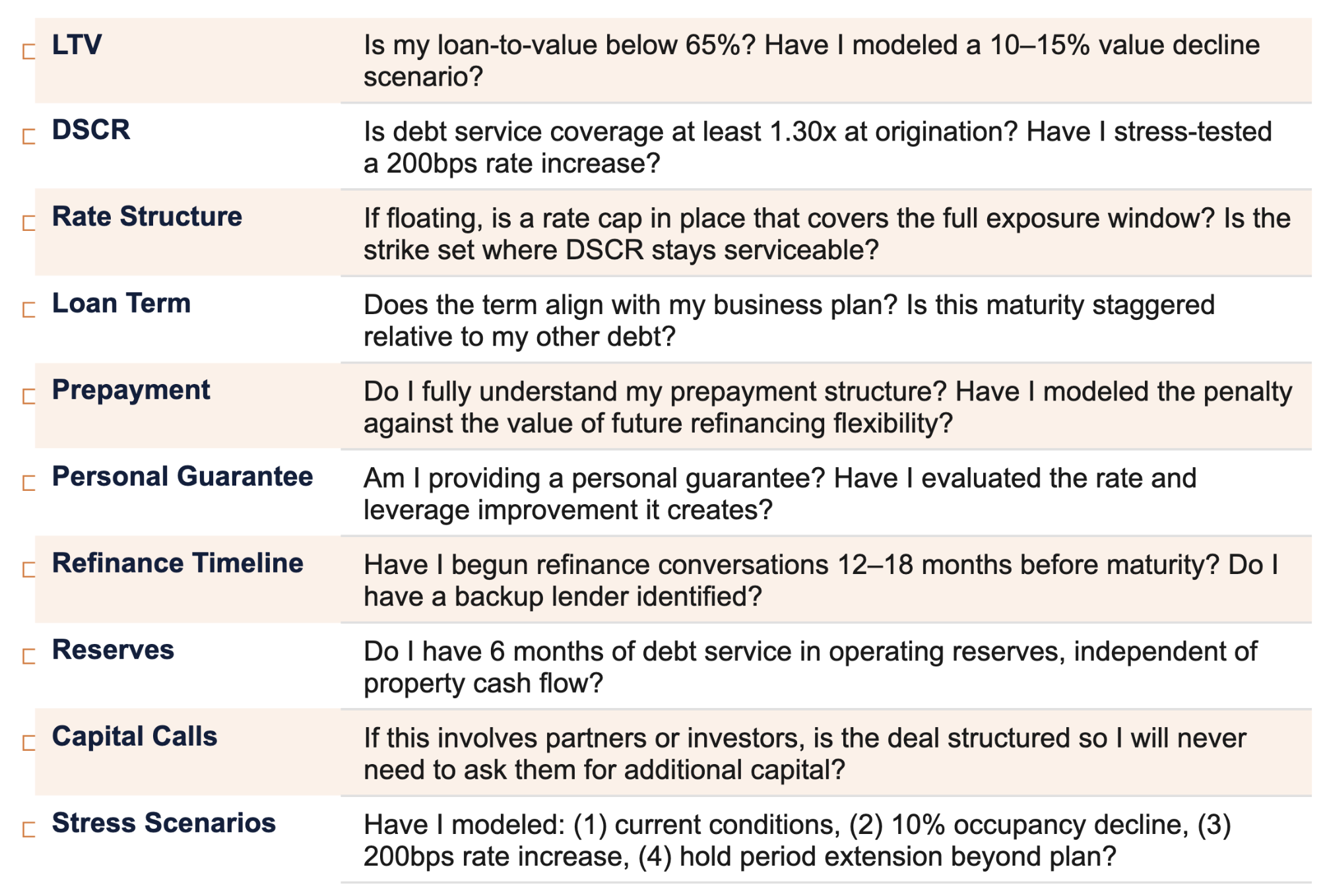

The Self Storage Financing Checklist

Work through each of these before committing to any loan structure on an acquisition or refinance. The questions that feel tedious before closing are the ones that matter most after.

The Operators Who Thrive Are Positioned Before the Market Moves

Self storage is one of the most resilient commercial real estate categories available to private investors. Demand is driven by life transitions - moves, business changes, downsizing, growth - that happen regardless of economic conditions. The asset class has outperformed broader commercial real estate across multiple decades and multiple cycles.

What separates consistently strong operators from occasionally strong ones is not the ability to predict market conditions. It is the discipline to build capital structures that work across conditions: conservative enough to absorb stress without asking partners to absorb it for you, flexible enough to act when opportunity appears, and aligned enough that every decision-maker in the deal is rowing in the same direction.

The financing decisions you make at acquisition are the ones you live with through the full market cycle. Make them with the bottom of the cycle in mind, and the top will take care of itself.