For the past few years, one idea has dominated almost every conversation I’ve had about commercial real estate debt:

Just wait for rates to come down.

I’ve heard it from investors, owners, brokers, and developers. The assumption has been that today’s higher borrowing costs are temporary and that, eventually, the Federal Reserve will cut rates enough for refinancing conditions to return to something closer to what we experienced before 2022.

I understand why people want to believe that.

If you purchased a storage facility with debt at 3.5% or 4%, refinancing that same property at 6% or 7% can completely change the economics of the investment. Even if the property is performing reasonably well, the higher debt service can significantly reduce cash flow and create problems with debt service coverage requirements.

So naturally, many owners have chosen to wait. They have extended loans when possible, purchased rate caps, negotiated with lenders, or simply held onto the belief that cheaper money was right around the corner.

But the bond market is currently telling us a very different story.

Over the past seven months, long-term interest rates have not fallen. In fact, they have moved higher. The 10-year Treasury increased from 4.14% in November 2025 to 4.46% in June 2026, while the 30-year treasury moved from 4.74% to 4.94%.

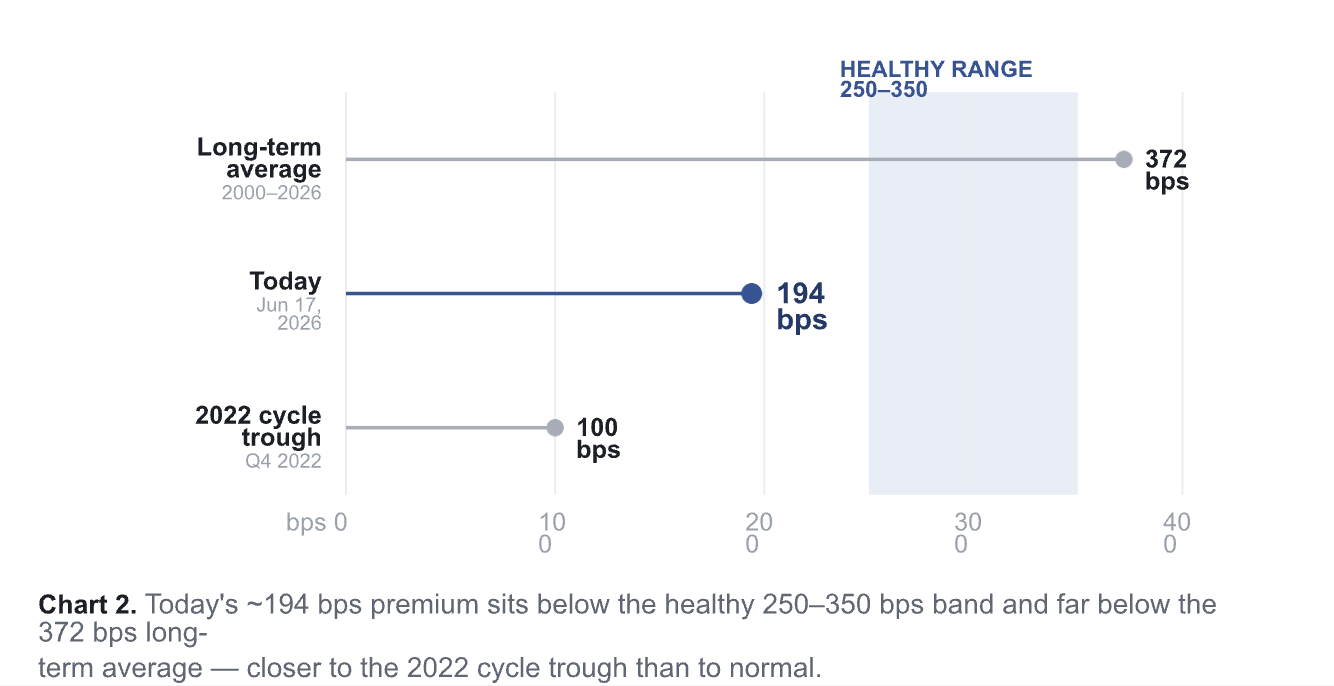

At the same time, the spread between storage cap rates and the 10-year Treasury has compressed to roughly 194 basis points, compared with a long-term average of approximately 372 basis points.

That matters enormously for anyone buying, selling, financing, or refinancing a self storage facility.

The market is sending a message, and I think every storage investor needs to understand what it means. Today, we’re going to dive into this.

The Yield Curve Is Not Doing What Investors Expected

There is a common misconception about interest rates that I see constantly in real estate.

People assume the Federal Reserve directly controls the interest rate on their commercial real estate loan.

It doesn’t work that way.

The Fed has significant influence over short-term rates, but longer-term borrowing costs are heavily influenced by the bond market. When lenders price five-, seven-, or ten-year commercial real estate debt, the longer end of the Treasury curve matters tremendously.

Over the past seven months, the front and long ends of the curve have behaved differently.

The 3-month Treasury moved slightly lower, from 3.89% to 3.76%. However, the 2-year Treasury increased from 3.62% to 4.06%, the 10-year increased from 4.14% to 4.46%, and the 30-year increased from 4.74% to 4.94%.

What stands out to me is the difference between what many investors expected and what actually happened. The common assumption was that easing at the front end of the curve would eventually pull borrowing costs lower across the board. Instead, investors demanding compensation for longer-duration risk pushed those yields higher.

There are several reasons for this. Inflation concerns have remained persistent, fiscal deficits continue to put pressure on the bond market, and the Federal Reserve remains constrained in how aggressively it can ease monetary policy when inflation is elevated.

The important point for a storage investor is simpler: you cannot build an investment strategy around the assumption that long-term borrowing costs will automatically fall because the Fed eventually cuts short-term rates.

Those two things are related, but they are not the same.

If your entire refinancing strategy depends on a dramatic decline in long-term rates, you are making a macroeconomic bet with your property. I don’t like building business plans around things I cannot control.

The Most Important Number Isn’t the Cap Rate

Self-storage investors spend a tremendous amount of time talking about cap rates.

Is this a 6 cap market? Will cap rates compress? What will my exit cap rate be in five years?

Those are important questions, but I believe there is another number that deserves just as much attention: the spread between the property cap rate and the 10-year Treasury.

Think about this from the perspective of capital.

If an investor can buy a relatively low-risk government bond at an attractive yield, how much additional return do they need to justify owning an operating real estate asset?

Real estate comes with work and risk. You have tenants, employees, insurance, taxes, maintenance, competition, capital expenditures, and operational execution. Investors need to be compensated for taking those additional risks.

Historically, the spread between storage cap rates and the 10-year Treasury has averaged roughly 372 basis points. A healthier range has generally been somewhere around 250 to 350 basis points.

Today, that spread is approximately 194 basis points.

This is one of the most important charts in the entire report because it shows the tension that still exists in the market.

At roughly 194 basis points, the current premium is significantly below the long-term average of 372 basis points and also below the 250–350 basis point healthy range.

That does not automatically mean property values have to collapse. It does mean the relationship eventually needs to normalize through some combination of lower Treasury yields, higher cap rates, and NOI growth.

This is why I would be extremely careful underwriting aggressive cap-rate compression as a base-case assumption today. If compression happens, great. That becomes upside.

But I do not want the success of my investment to depend on a macroeconomic outcome that I cannot control.

What Has Already Happened to Storage Values

The storage market reached extraordinary valuations during the last cycle.

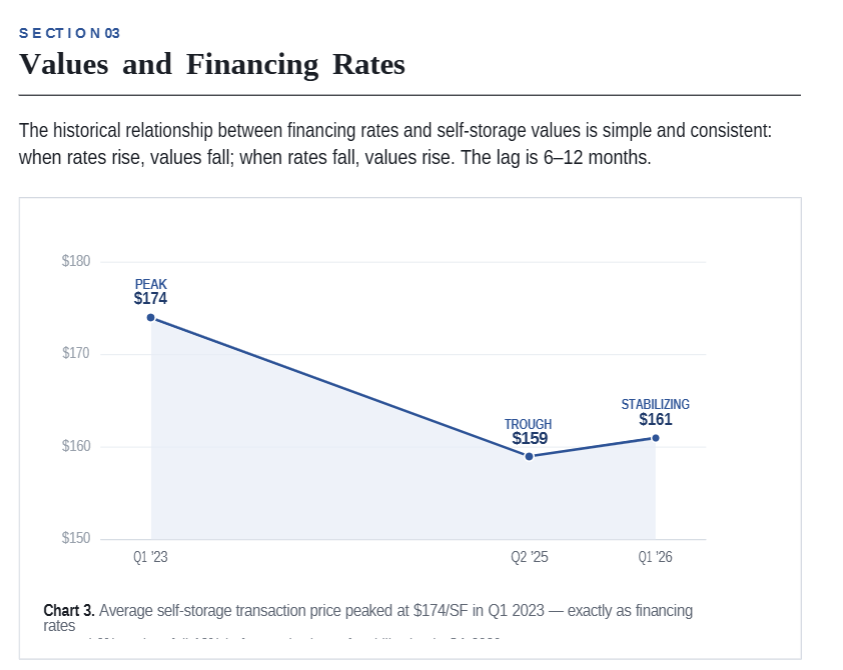

Average transaction pricing reached approximately $174 per square foot in the first quarter of 2023. By the second quarter of 2025, that figure had declined to roughly $159 per square foot, with early signs of stabilization appearing around $161 per square foot in the first quarter of 2026.

On a broader valuation basis, self storage asset values declined approximately 25% from their 2022 peak. Among major commercial real estate sectors, only office experienced a larger correction.

This is where I think investors need to separate a price correction from a broken business model.

Storage values have experienced a meaningful reset, but construction costs have simultaneously risen substantially since 2020. The cost of building new self storage is up approximately 40% to 60% in many markets.

That has created an unusual situation where existing facilities can sometimes be acquired at or below the cost of building a competing property from the ground up.

For me, that is where this market becomes interesting.

I don't want to buy an asset simply because its price has fallen. A falling price does not automatically create value. I want to buy an asset at an attractive basis where replacement cost, demonstrated demand, and operational upside create a margin of safety.

Those are very different things.

The Refinancing Wall Is the Real Story

The broader commercial real estate market is approaching an enormous wave of loan maturities.

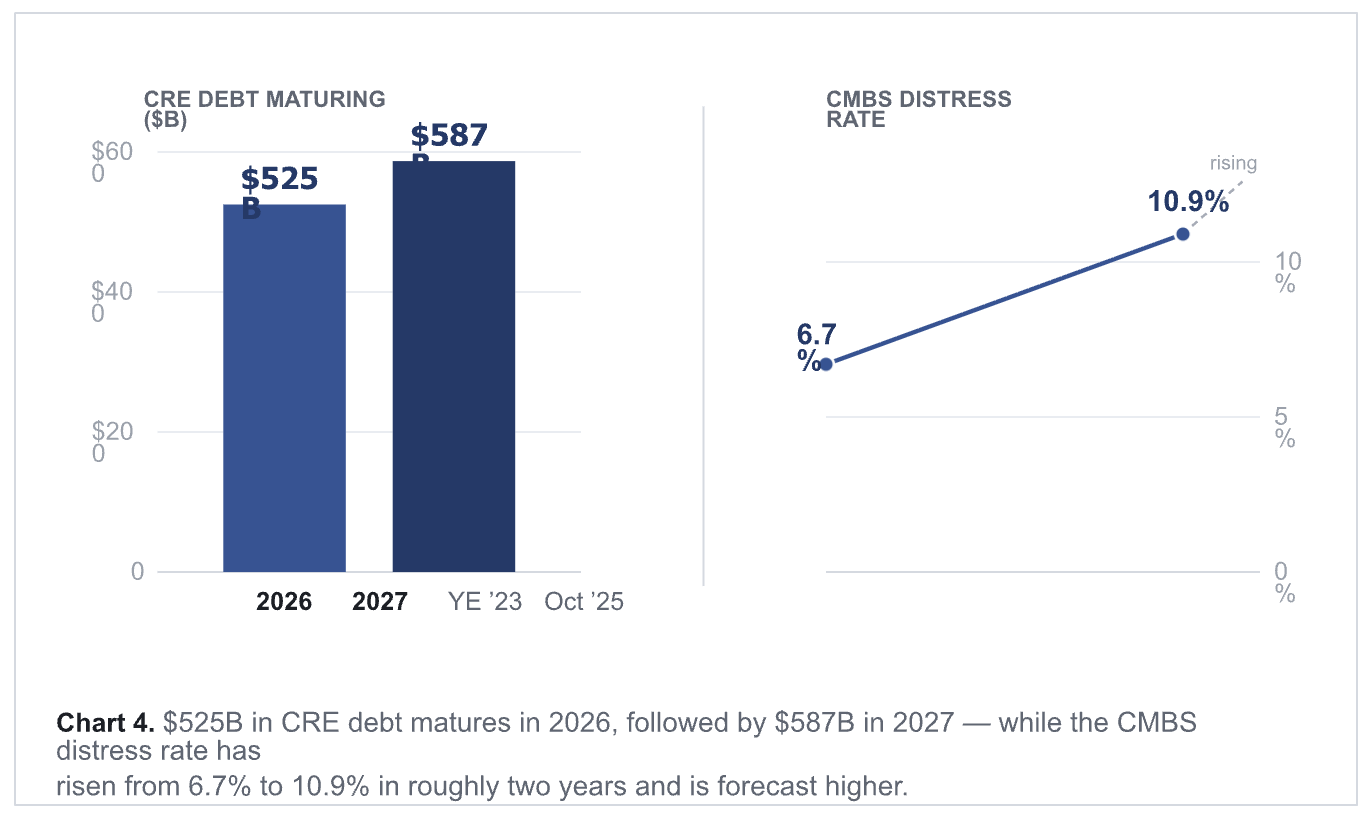

Approximately $525 billion in commercial real estate debt is scheduled to mature in 2026, followed by another $587 billion in 2027.

Together, those two years represent more than $1.1 trillion in commercial real estate debt coming due.

Not all of that debt is self storage, of course, and storage is fundamentally different from the office sector. But all commercial real estate borrowers compete within the same broader capital markets.

When hundreds of billions of dollars of loans need to be refinanced, lenders become more selective. Capital gets allocated toward the strongest borrowers and assets, while weaker capital structures become exposed.

This is particularly important for investors who purchased properties between 2020 and 2022.

Imagine that you purchased a facility during that period using 60% or 65% leverage against a peak valuation. The property may not have collapsed operationally. Perhaps NOI is stable or even slightly higher.

But the value of the asset may have fallen while the cost of refinancing has increased dramatically.

A loan that represented 65% of value when originated could effectively represent a much higher percentage of today's property value. At the same time, replacing a 3.5% or 4% loan with debt costing 6% or 7% creates significantly higher annual debt service.

That combination is the refinancing gap.

And it is one of the places where I expect opportunities to continue emerging.

A Simple Test Every Owner Should Run

If you own a self storage facility with a loan maturing in the next few years, I think there are a few calculations you should be running right now.

First, take your current NOI and divide it by your outstanding loan balance. This gives you a simple measure of debt yield.

If that debt yield is below 8%, you may have a meaningful refinancing gap. Even below 10%, I would want to understand exactly how much cushion exists in the deal.

Second, calculate your DSCR using a realistic refinancing rate rather than the rate you hope to receive. Run the property at 7% debt and see what happens.

Can the property still produce at least 1.25x debt service coverage?

If not, you may not be able to refinance the existing balance at par. That could mean contributing additional equity, negotiating with the existing lender, finding a new capital partner, or selling the property.

The mistake is waiting until 60 days before maturity to discover that problem.

I would rather understand the gap two years early and have ten potential solutions than discover it two months early and have one bad option.

Watch What the Institutions Are Doing, Not What People Are Saying

One of the most interesting parts of this market is the difference between what people are predicting and what the largest institutional storage operators are actually doing.

I always pay attention to behavior over predictions.

Public Storage recently chose to issue long-duration fixed-rate debt rather than simply waiting and hoping that rates would fall. According to the research, the company priced a $500 million offering of 5% senior notes due in 2035.

Think about what that means.

One of the largest and most sophisticated storage operators in the world was willing to pay 5% to secure long-term fixed-rate capital. They have access to the same economic forecasts everyone else sees, and their decision was to remove uncertainty rather than speculate on future rate cuts.

Extra Space Storage has taken a similar approach to interest-rate risk. According to the research, 82.5% of its debt is fixed-rate, and after accounting for variable-rate receivables and hedging, its effective fixed-rate position is approximately 92.9%.

Again, look at the behavior.

The institutions aren't structuring their balance sheets around hope. They're paying to remove variability.

Even more interestingly, some institutions are moving to the other side of the table and becoming lenders.

The report notes that Public Storage originated $48.4 million of bridge financing for third-party owners in the fourth quarter of 2025 at an average rate of 7.7%. At the same time, it was able to access long-term capital at approximately 5%.

That is a fascinating strategy because distress creates opportunity in more than one way. You can acquire discounted assets, but if you have access to capital, you can also provide financing to operators who do not.

The strongest capital structures become increasingly valuable when liquidity is constrained.

Should You Lock Your Rate or Wait?

This is probably the question I hear most frequently.

The answer depends heavily on your maturity date and the specific economics of your facility, but I believe owners with loans maturing in 2026 or 2027 need to be proactive.

Waiting for the perfect rate can be extremely expensive if it turns you into a forced borrower or forced seller.

A borrower with time has options. A borrower facing a maturity deadline has whatever options the market is willing to provide.

For loans maturing later, particularly in 2028 or 2029, there is more flexibility. But flexibility should not be confused with certainty. Owners may want to evaluate partial fixed-rate strategies, hedges, or other structures that reduce exposure without completely eliminating future upside if rates decline.

The broader lesson is that debt strategy should be intentional.

Debt is not just a line item in your underwriting model. It is one of the biggest risks in commercial real estate because the asset is long-term while the debt often is not.

You may plan to own a facility for 20 years, but your loan could mature in five.

That mismatch has to be managed.

Is This a Risk or an Opportunity?

My answer is both.

There is real risk for owners with near-term maturities, floating-rate debt, weak debt coverage, or properties in markets still absorbing significant new supply.

At the same time, those conditions are exactly what create opportunities for disciplined buyers.

My investment framework in this environment comes down to three things.

First, I want to buy below replacement cost. If I can acquire an existing facility for less than it would cost a competitor to build a new one, that creates an important structural advantage.

Second, I want demonstrated demand. I am not interested in speculative demand projections that require everything to go perfectly. I want markets where the underlying demand drivers can be verified.

Third, I want operational systems ready on day one. Distressed assets are not automatically good investments. If a facility has poor revenue management, weak digital marketing, bad collections processes, or ineffective management, the buyer needs the systems to fix those problems immediately.

That is why I believe this is an operator's market.

The next cycle will not reward everyone equally. Simply owning a storage facility is not enough. Capital structure, basis, operational execution, and market selection are becoming increasingly important.

The Next 18 to 24 Months

I believe the next 18 to 24 months could be extremely important for the self storage industry.

There are owners facing refinancing gaps at the same time that asset values have already corrected significantly. New development economics are more difficult because construction costs remain elevated, and in many markets existing facilities can be purchased below replacement cost.

Meanwhile, the strongest institutional players are locking in duration, hedging variable-rate exposure, and positioning themselves to provide capital to operators under pressure.

That tells me something.

The sophisticated capital in our industry is not sitting around waiting for someone to announce that the market is safe again. It is positioning itself for what comes next.

I think private investors should pay attention to that lesson, even if the scale of their strategy is completely different.

You don't need billions of dollars or access to public debt markets. But you do need to understand your maturities, protect your cash flow, maintain liquidity, and know exactly where your opportunities will come from.

For years, cheap money covered up a lot of mistakes. When debt was available at 3% or 4%, almost every problem had the same solution: refinance.

That world has changed.

The investors who understand their capital structure will have options. The ones who have fixed-rate capital, dry powder, and strong operating systems will be able to acquire assets from owners who waited too long to confront reality.

I have been through enough market cycles to know that the greatest opportunities rarely arrive when everyone feels comfortable.

They arrive when the math becomes difficult, when financing becomes constrained, and when good assets become available because the owner has a capital problem rather than a real estate problem.

That is the environment I am watching today.

The bond market is telling us that the easy refinancing environment may not return on the timetable many investors expected. The largest institutions in our industry are acting accordingly, and I believe private operators should be doing the same.

Not by panicking or trying to predict every Fed meeting or Treasury move, but by understanding the debt, protecting the downside, and being prepared to act when the right assets come to market.

Because the next 18 to 24 months will likely separate the investors who were dependent on cheap capital from the operators who know how to create value in any capital environment.

And historically, that separation is where some of the greatest wealth-creation opportunities begin.

That's it for now. Stay tuned for next time.

- AJ