Are you like me - do you like making jokes about your generation, and the ones that came before and after you?

As a first year Millennial, I’ve certainly taken a lot of heat. I’m sure you know all the sayings about my generation, no need to repeat here.

But jokes and stereotypes aside, there’s been a lot of talk online about how previous generations - Baby Boomers in particular - had it “easier” than their later counterparts.

Is that true? Are Boomers really better off than Millennials?

In today’s email, I’m going to separate fact from fiction. I’ll break down the data behind the generational wealth gap, exploring regional economic disparities, rising home prices, and the role of interest rates in shaping financial realities.

Alright, let's get to it.

1. Millennials’ Wealth Today: The Reality Behind the Numbers

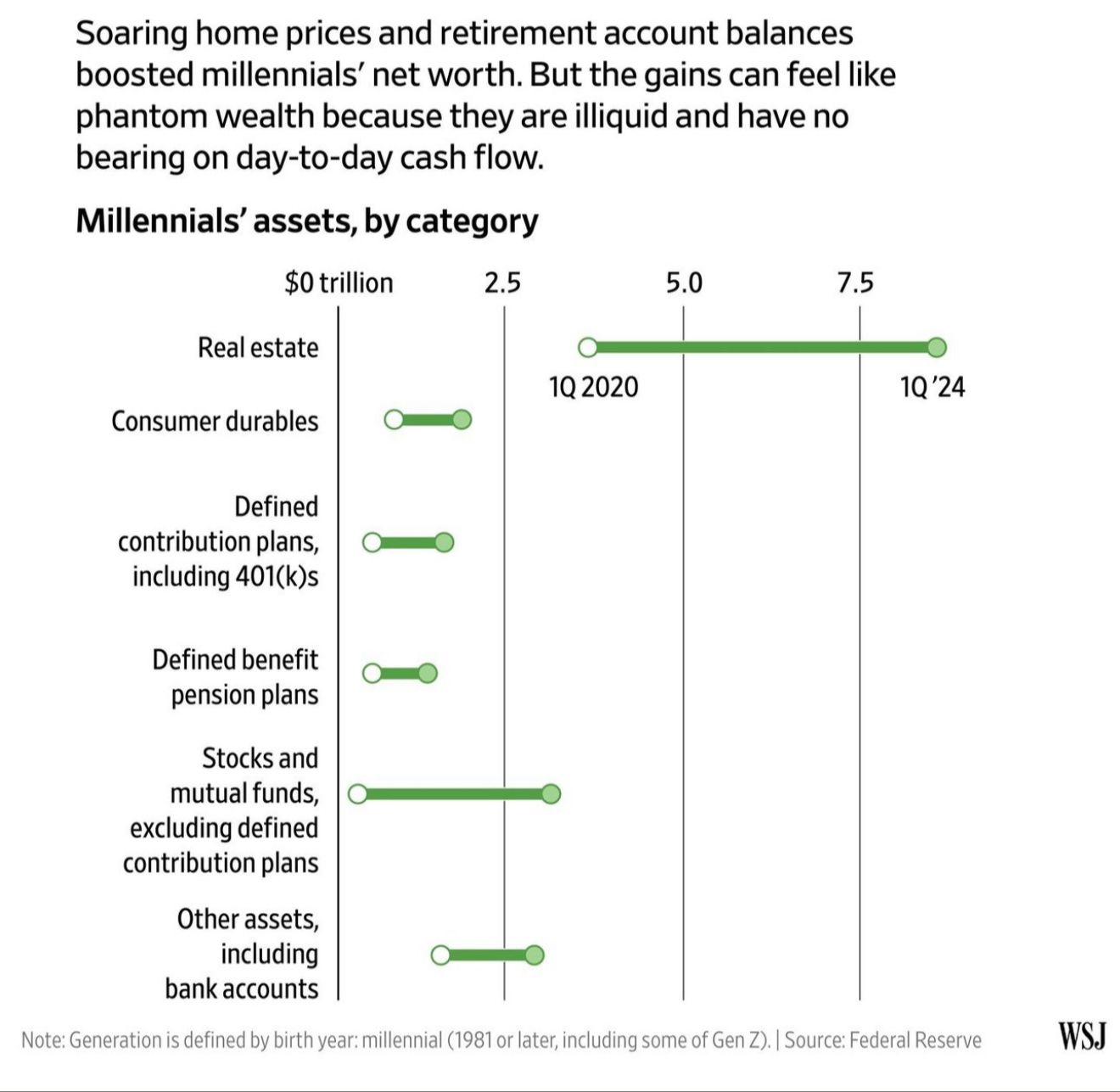

The Wall Street Journal recently published that Millennials today hold 25% more wealth than Baby Boomers or Gen Xers did at a similar age when adjusted for inflation. While this statistic may seem promising, the broader context paints a different picture:

- Economic Challenges: Millennials face unprecedented hurdles, such as skyrocketing home prices, overwhelming student debt, and wages that have struggled to keep pace with inflation. These challenges are compounded by economic instability stemming from the 2008 financial crisis and the COVID-19 pandemic.

- Delayed Milestones: Unlike previous generations, Millennials have delayed key life milestones, such as marriage, homeownership, and having kids. These delays significantly impact wealth accumulation, particularly in markets where asset ownership drives long-term financial stability.

2. Geography’s Role in Wealth Creation

Turns out, the financial reality of Millennials versus Baby Boomers is deeply influenced by geography. Population growth in states like Texas, Florida, and Idaho has driven up home prices and created wealth opportunities for those who already owned property in these regions.

That said, in areas with low or negative population growth, home values have stagnated or even declined, leaving residents with fewer opportunities to build wealth. There’s also huge regional disparities - the economic boom experienced in high-growth states illustrates how wealth creation can be disproportionately distributed based on location.

3. Lifestyle and Spending Patterns Across Generations

The way Millennials and Baby Boomers structure their lives has shifted dramatically, influencing their financial trajectories:

- Household Size and Homeownership: Baby Boomers at age 30 typically lived in smaller homes (1,700 square feet on average) with larger households. In contrast, Millennials inhabit larger homes (2,400 square feet on average) with fewer occupants. This shift reflects changing cultural values but also higher costs per person.

- Marriage and Family: In 1983, approximately 80% of individuals at age 30 were married, compared to just 40% of Millennials today. Marriage and family life, historically linked to wealth-building through dual incomes and homeownership, are far less common among Millennials.

4. The Influence of Interest Rates and Inflation

Interest rates play a pivotal role in shaping the financial experiences of these two generations:

Baby Boomers experienced high interest rates throughout much of their early adulthood, with rates often exceeding 8-9%. While borrowing was expensive, high rates also provided opportunities for savings and wealth accumulation over time.

Conversely, most Millennials entered adulthood during a period of historically low interest rates, which, while making borrowing cheaper, also spurred rapid asset price inflation. Homes, stocks, and other assets became increasingly unaffordable, particularly for younger Millennials who missed earlier investment opportunities.

Inflation has further exacerbated these challenges. Recent government spending and monetary policies have devalued the dollar, driving up prices for essentials like housing, food, and education. As a result, Millennials entering the workforce in the past decade face significantly higher costs than their Baby Boomer counterparts did at the same age.

So, some of that online hype about “Boomers having it better” is true - at least in terms of the cost of necessities.

5. Asset Ownership: The Key to Wealth Creation

Here’s the hard truth: owning assets (like homes or stocks) is one of the biggest drivers of wealth. Boomers benefitted hugely from rising home prices and stock market growth.

For Millennials, it’s been more of a mixed bag. After the 2008 crash, many of us were hesitant to buy homes, and by the time we felt ready, prices had skyrocketed. Those of us who did invest early (2008-2016) scored big, but not everyone had the means or confidence to take that risk.

The reality is that generational wealth isn’t just about age. It’s also about timing, geography, and opportunities. Some Millennials who lived in fast-growing areas or invested early have done great. Others, especially in high-cost areas or those hit hard by inflation, feel like they can’t catch a break.

And let’s not forget: Boomers had their own struggles. They dealt with high inflation and interest rates for decades, and many were hit hard during the 2008 financial crisis.

Final Thoughts

So, are Millennials better off than Boomers? Honestly, it depends. The one big takeaway is this: owning assets (homes, stocks, businesses) has always been a winning strategy. The challenge for us is figuring out how to get there in today’s crazy economy.

The good news? Us Millennials have tools that Boomers didn’t, like YouTube and other social media platforms, plus communities that share knowledge. With the right mindset and strategy, there are still opportunities out there.